|

29.06.2020 15:59:03

|

Schroders: Moving from recession to recovery: how can investors position themselves?

So how should investors manoeuvre their portfolios as the economic cycle moves from recession into recovery? This is where an understanding of the stages of the cycle can be an useful guide to asset allocation. While historical returns using the economic cycle is no guarantee of the future path, there is a reassuring rhythm to the performance.

Minding the gap

In defining the stages of the economic cycle, we rely on the Schroders US output gap. Simply put, the output gap measures the difference between the actual and potential output of the economy (measured using GDP). To measure the output gap, we use the unemployment rate and the capacity utilisation rate versus their long run trends.

In the chart above, the cycle has slipped firmly into the recession phase with the output gap plunging into negative territory. A move into recovery would mean that the output gap needs to narrow - that is, turn less negative - compared to three months ago. While the market appears to have already priced in a recovery, our model suggests that this is likely to occur in Q4 this year, based on the Schroders Economics team’s baseline forecasts.

What do the recession and recovery phases mean for multi-asset investing?

In the recession phase, the credit class typically shines, particularly high yield. This is because, as companies repair their balance sheets and markets anticipate a rebound in the economy and corporate earnings, the prices of these bonds rise (meaning yields fall). This backdrop also helps equities to recover, although investors tend to favour credit in this environment. Besides being a more defensive asset, the higher yield from owning credit is being supported by accommodative monetary policy by the Federal Reserve (Fed). Compared to the Fed’s support in the wake of the global financial crisis (GFC), credit is this time being further boosted by unprecedented levels of corporate bond buying.

As investors become more confident that the cycle has moved into the recovery phase - with stronger growth, but still muted inflation - equities typically outperform credit. Interestingly, during the recovery phase, equities are not driven by a re-rating in the market. Re-rating is a change in the amount investors are willing to pay for a company relative to its earnings, or the "price-earnings ratio".

Instead, equities in the recovery phase are driven by stronger growth in earnings, or specifically earning per share (EPS). Most of the re-rating in the market predominately occurs during recessions, while EPS growth is negative. However, the challenge this time around is that valuations are starting from a higher level which means there is less of a re-rating cushion compared to past recessions.

Table 1: Performance stats of US equities during recessions and recoveries

Meanwhile, the better growth landscape in the recovery phase fails to lift the overall commodity complex, which also delivers dismal returns during recessions. This is driven by the lacklustre performance of the sectors that are most sensitive to the cycle, such as industrial metals and energy.

Nonetheless, there is still scope for investors to add commodities in the recovery phase. The improvement in economic activity with - monetary policy remaining accommodative - has led to some gains in industrial and precious metals. The caveat to these findings is that it is based on the US cycle and we have not taken into consideration the China cycle. For instance, China accounts for half of world’s copper consumption, which represents 40% of the GSCI industrial metals index.

Table 2: Commodity returns by sector based on the cycle

US dollar - the ultimate safe-haven currency during recessions?

The "greenback", measured by the DXY index, has been the ultimate currency for investors to hide in during past recessions. Safe-havens currencies such as the Japanese yen (JPY) and Swiss franc (CHF) have also faired better relative to other G10 currencies during downturns. By contrast, the higher beta currencies or those currencies most geared to the strength of the economic cycle have been the performance laggards.

In the recovery phase, investors have generally fallen out of love with the US dollar and rotated into the riskier currencies. At the same, they have kept some safe-haven currency bets in the portfolio judging by the past performance of the JPY and CHF in recoveries.

With the changing of the cycle, it is all about sectors and style

Despite recessions being underpinned by low growth prospects, investors have favoured the consumer-oriented sectors relative to the overall market. While consumer staples are clearly defensive in nature versus the consumer discretionary sector, both segments have outperformed in recessions. This is likely due to the market discounting households receiving a boost in disposable income from lower inflation, oil prices and interest rates. Lower interest rates also help steepen the yield curve during recessions, which improves the profitability of financial companies. Specifically, this means they can receive income on loans based on higher long-terms rates but pay deposits using lower short-term rates.

In comparison, nearly all of the cyclical names such as tech, communications and energy have been left behind by the S&P 500 during recessions. However, there is a general reversal in sector leadership in the recovery phase with the more cyclical areas of the market doing well such tech and industrials.

In terms of US equity styles, the more defensive areas such as growth/quality stocks, and companies with high dividend yield do well in recessions. Despite their cyclicality, small caps have surpassed their larger peers in the performance stakes. This is because investors are anticipating the recovery in corporate profitability of these companies, which are more sensitive to falling interest rates and the expansion of liquidity from the central bank.

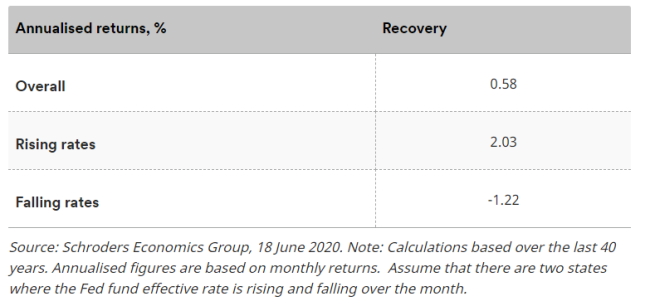

By contrast, recessions have typically been the worst periods for value stocks, given the weak growth and muted inflationary backdrop. However, in the recovery phase, the value trade has typically regained its spark beating the broader market, particularly when the Fed is hiking interest rates. It would appear that value stocks looking "cheap" are less impacted than their more expensive quality/ growth counterparts by the higher discount rate on earnings.

Table 3: US value premia shines during recoveries when interest rates are rising

Can we say anything about alternative assets based in the cycle?

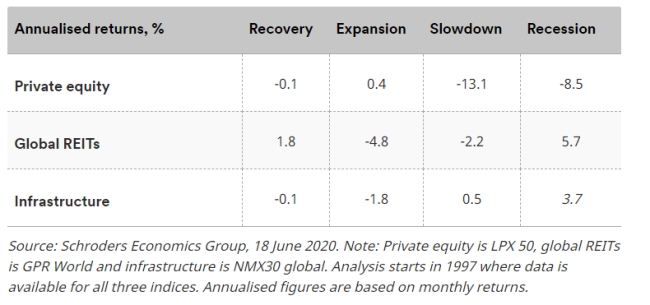

Most of the analysis looking at the performance of markets based on the economic cycle has been concentrated in the traditional asset classes. Similar examination of alternative assets is partly hindered by the lack of back-history to measure the return profile over several cycles. Nonetheless, over the last 20 years, we find that listed global REITs and infrastructure deliver stronger returns relative to global equities during the recession phase. These steady, income generating parts of the market appear to be more resilient to the downturn in economic activity. In the recovery phase, there is less of a distinction between these listed alternatives compared to global equities.

Table 4: Listed global alternatives compared to MSCI AC World

How is this cycle shaping up compared to the past?

So far, the performances of some of the key markets in this recession (starting in February) are following a slightly different rhythm compared to past economic downturns. In particular, US government bonds have beaten their riskier peers such as US equities and high yield. Meanwhile, commodities has proved to be one of the worst assets to own during previous recessions, although the sharp drop in prices is particular severe compared to past cycles.

In terms of styles, growth has outperformed value which is in-line with past recession phases. However, the magnitude of returns are higher so far in this recession. Among the sectors, unusually tech has delivered strong returns while consumer staples has underperformed.

Conclusion

In the recovery phase, equities have historically warranted a higher allocation in the portfolio versus credit as this asset class has tended to benefit from stronger earnings growth. Looking ahead, we need to see a recovery in earnings, as there is a limit to the re-rating in the price earnings ratio, which has driven the latest rally in the equity market.

At the same time, there is a stronger argument for credit in the portfolio as monetary policy remains accommodative, particular with the Fed buying corporate bonds. On commodities, unlike previous recoveries, there is scope to allocate more weighting towards this asset particularly given the severity of underperformance in this recession.

Meanwhile, investors should think about shifting their overweight allocations in the US dollar to riskier currencies but keep some defensive currencies.

In terms of US sector performance during recoveries, the more cyclical areas of the market - such as tech and industrials - have tended to do well. While there is more valuation support for the more cyclical names, tech has unusually delivered stellar returns during this recession, which may curtain their sparkle compared to previous recoveries. Moreover, the value trade has generally outperformed in this phase, although this may prove to be more challenging, with the Fed expected to keep rates at rock bottom for an extended period. Overall, the main takeaway for investors is that there is a more pro-cyclical flavour to asset allocation during the recovery phase.

You can find more Insights articles here: https://www.schroders.com/de/ch/asset-management/insights/

Important Information: This communication is marketing material. The views and opinions contained herein are those of the author(s) on this page, and may not necessarily represent views expressed or reflected in other Schroders communications, strategies or funds. This material is intended to be for information purposes only and is not intended as promotional material in any respect. The material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. It is not intended to provide and should not be relied on for accounting, legal or tax advice, or investment recommendations. Reliance should not be placed on the views and information in this document when taking individual investment and/or strategic decisions. Past performance is not a reliable indicator of future results. The value of an investment can go down as well as up and is not guaranteed. All investments involve risks including the risk of possible loss of principal. Information herein is believed to be reliable but Schroders does not warrant its completeness or accuracy. Some information quoted was obtained from external sources we consider to be reliable. No responsibility can be accepted for errors of fact obtained from third parties, and this data may change with market conditions. This does not exclude any duty or liability that Schroders has to its customers under any regulatory system. Regions/ sectors shown for illustrative purposes only and should not be viewed as a recommendation to buy/sell. The opinions in this material include some forecasted views. We believe we are basing our expectations and beliefs on reasonable assumptions within the bounds of what we currently know. However, there is no guarantee than any forecasts or opinions will be realised. These views and opinions may change. The content is issued by Schroder Investment Management Limited, 1 London Wall Place, London EC2Y 5AU. Registered No. 1893220 England. Authorised and regulated by the Financial Conduct Authority.

Fondsfinder

Meistgelesene Nachrichten

finanzen.net News

Börse aktuell - Live Ticker

US-Börsen schliessen in der Gewinnzone -- SMI und DAX gehen höher ins Wochenende -- Asiens Börsen letztlich freundlichDer heimische sowie der deutsche Aktienmarkt verzeichneten zum Wochenende Gewinne. Die Wall Street legte deutlich zu. An den Börsen in Asien ging es am Freitag nach oben.